Oil Freight Rates in the Strait of Hormuz Continue to Rise

RoydadNaft – Experts say the ceasefire will not reduce oil shipping costs through the Strait of Hormuz for the time being.

According to Roydad Naft, the latest assessment by shipping industry experts shows that although oil tanker traffic through the Strait of Hormuz is gradually resuming after the ceasefire between Iran and the United States, the maritime transport market is still feeling the effects of the war, and a full return to pre-crisis conditions will take time.

According to the report, the initial peace agreement signed between Iran and the United States on June 17 paved the way for mine clearance operations and the resumption of vessel traffic in the Strait of Hormuz. This strategic waterway, through which about 20% of the world’s seaborne oil trade passes, experienced widespread disruption to shipping during the days of conflict.

Although crude oil and petroleum product exports are gradually recovering, analysts believe that security concerns, higher insurance costs, and new restrictions on passage through the Strait of Hormuz will remain the most significant factors affecting the oil transport market.

Strait of Hormuz: From a High-Capacity Artery to a Security Corridor

Fotios Katsoulas, a maritime transport analyst at S&P Global Commodity Insights, believes the most important change after the war is the transformation of the nature of the Strait of Hormuz. According to him, this waterway is no longer simply a free shipping route but has become a “security-managed corridor.” This means that even without a complete closure of the strait, security threats, intermittent disruptions, and an uncertain environment can severely reduce the operational capacity of vessels passing through it.

He emphasizes that the recent war showed that even without a full blockade, vessel traffic in some periods dropped to a small fraction of normal capacity.

Sharp Rise in War Risk Insurance for Oil Tankers

One of the most significant consequences of the war has been a dramatic increase in war risk insurance premiums for oil tankers. According to experts, war insurance rates on some routes have risen several times compared to pre-war levels, with the cost per voyage in some cases reaching several million dollars.

Analysts believe that war insurance is no longer just an additional expense but has become a decisive factor in whether shipowners enter the region or not. This has led to a reduction in the number of tankers operating in the area, longer voyage times, rerouting of vessels, and ultimately a surge in oil freight rates.

Sharp Increase in Oil Freight Rates

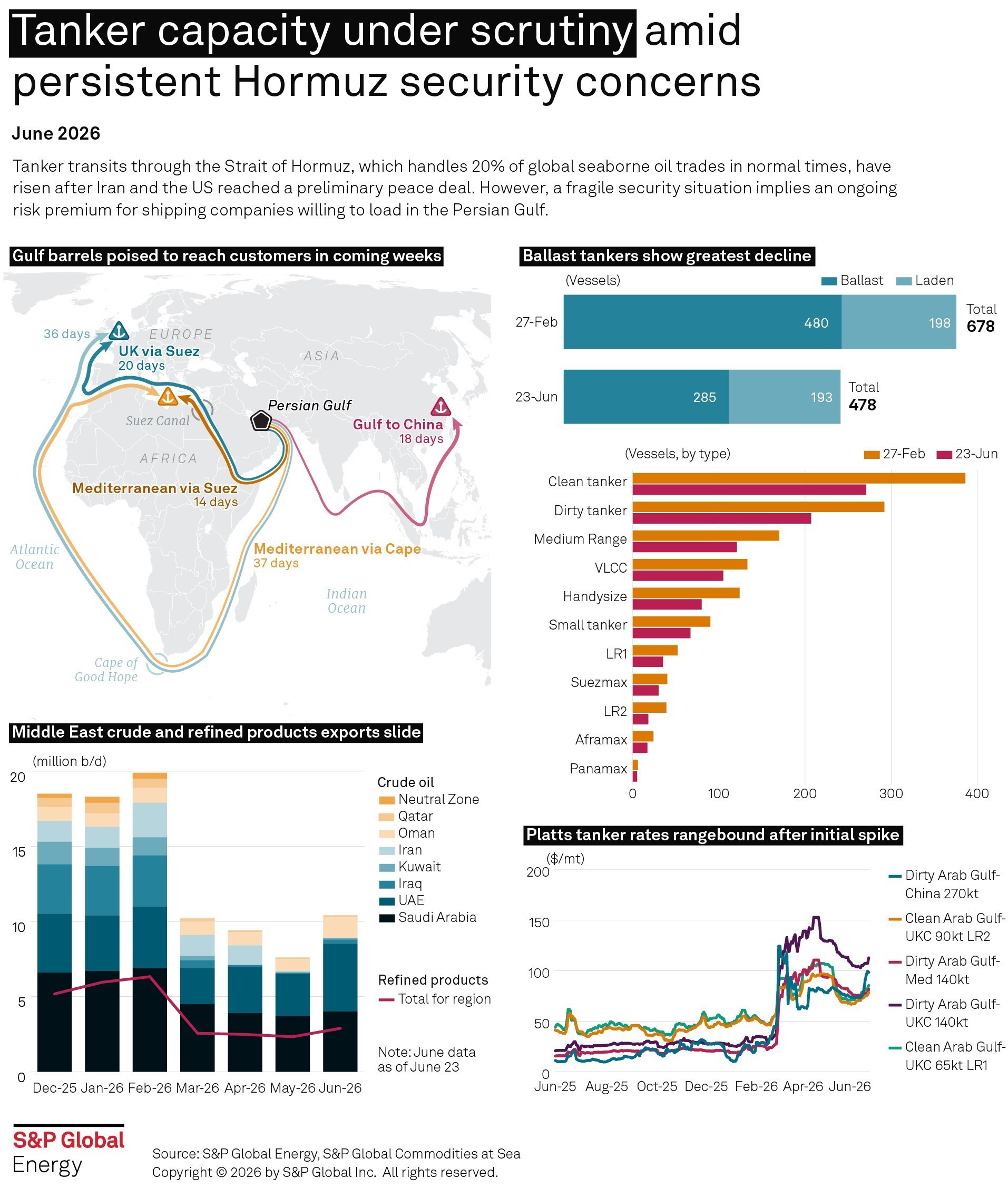

Platts assessments show that the cost of shipping a 270,000-ton crude oil cargo from the Persian Gulf to China reached $82.76 per ton on June 25 — compared to just $46.04 per ton on February 27, before the war began.

The cost of shipping a 65,000-ton petroleum products cargo from the Persian Gulf to Europe has also risen from $58.46 to $93.08 per ton, indicating a significant increase in maritime transport costs.

Limited Tanker Traffic in Hormuz

Currently, routes closer to the Omani and Iranian coasts are considered the safest passages, which has limited the daily capacity for tanker transits. According to Omani authorities, the country is working with the International Maritime Organization to establish a safe corridor for vessels that were stranded in the Persian Gulf during the war, but the number of daily transits will remain limited.

On the other hand, Iranian officials have stated that all vessel passages through the Strait of Hormuz are conducted under management and supervision, and ships require permits to transit — an issue that has increased operational requirements for shipping companies.

Reduced Entry of Ballast Tankers into the Persian Gulf

Experts also report a significant decline in the entry of empty (ballast) tankers into the Persian Gulf region. According to analysts, many shipowners are refraining from stationing their vessels in the area due to ongoing security uncertainties, so they can maintain greater flexibility in case of new tensions.

In some cases, insurance companies have canceled war risk coverage or raised premiums to levels that make the economic case for sending empty ships into the region unjustifiable.

Full Market Recovery Will Take Time

Shipping brokerage firm Gibsons has stated that although more very large crude carriers (VLCCs) have returned to the Persian Gulf in recent weeks, it will likely take two to three months for vessel supply to return to normal levels.

The firm predicts that with the gradual improvement in security conditions, tanker traffic through the Strait of Hormuz will increase slowly, and war risk insurance costs will decline in parallel. However, oil freight rates are expected to remain highly volatile.

Oil Storage Supports the Market

Analysts believe that another factor supporting the tanker market is countries’ need to rebuild oil inventories after the war. While countries usually build stockpiles when oil prices fall, this time — due to significantly depleted reserves and concerns over supply security — there is potential for increased precautionary buying, which could strengthen demand for oil transport.

Geopolitical Insurance Premium to Remain in Place

Experts believe that even with the full resumption of oil exports, the maritime transport market will continue to be affected by a “geopolitical insurance premium” for a long time. In their view, shipping companies and insurers will now permanently factor political and security risks into their contracts and pricing following the recent war experience — something that will prevent freight rates from quickly returning to pre-crisis levels.

Petroleum Products Market to Recover More Slowly

Meanwhile, experts predict that seaborne trade in petroleum products will improve more slowly than the crude oil market. According to Gibsons, damage to some Middle Eastern refineries means regional refining capacity will not return to pre-war levels until at least 2027.

Asian refineries will also be unable to increase production until feedstock supply returns to normal. As a result, seaborne trade in petroleum products is expected to remain below pre-war levels until late 2027.

The infographic from S&P Global Energy shows that although tanker traffic in the Strait of Hormuz has gradually resumed after the initial peace agreement, the maritime transport market continues to be affected by security risks. According to the report, the number of tankers in the Persian Gulf fell from 678 at the end of February to 478 on June 23, with the majority of the decline related to ballast (empty) tankers — indicating caution among shipowners about entering the region.

At the same time, crude oil and petroleum product exports from Middle Eastern countries have experienced a noticeable drop after the war, while tanker freight rates, after an initial surge, have stabilized at levels significantly higher than before the crisis. These figures show that despite the gradual reopening of the Hormuz route, high insurance costs, security restrictions, and reduced vessel supply continue to support elevated freight rates, and a return to normal market conditions will take time.